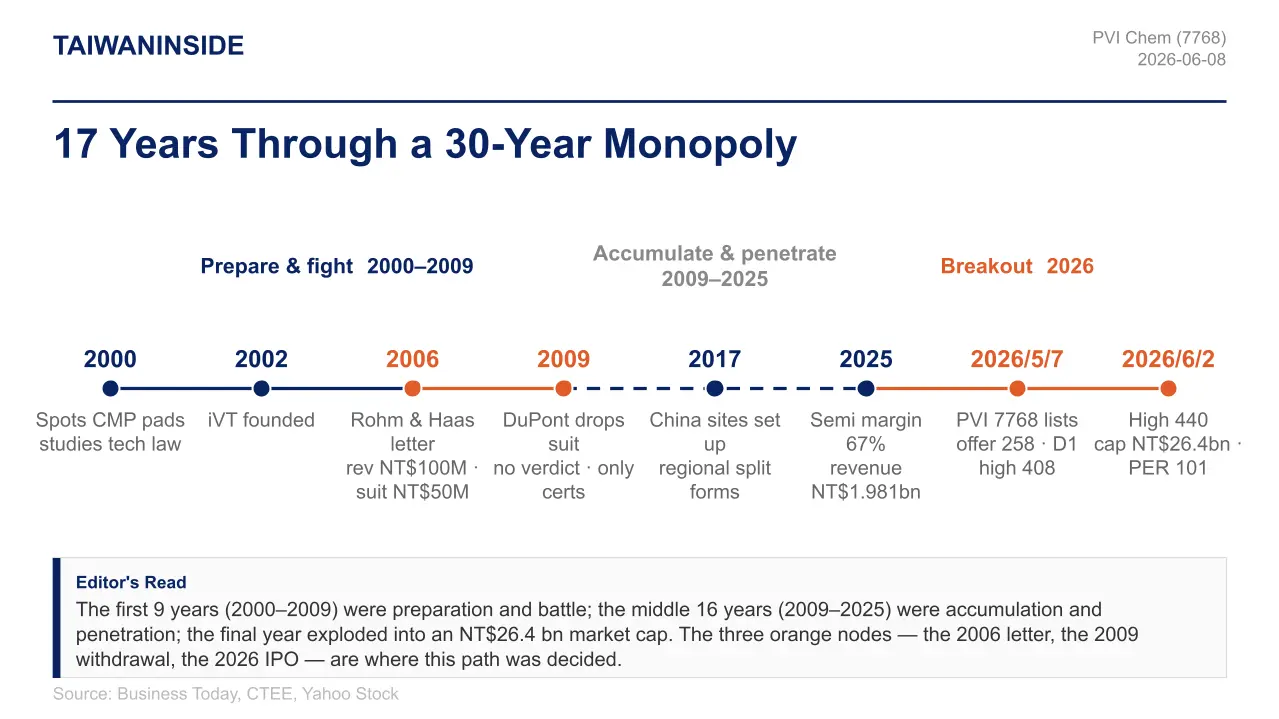

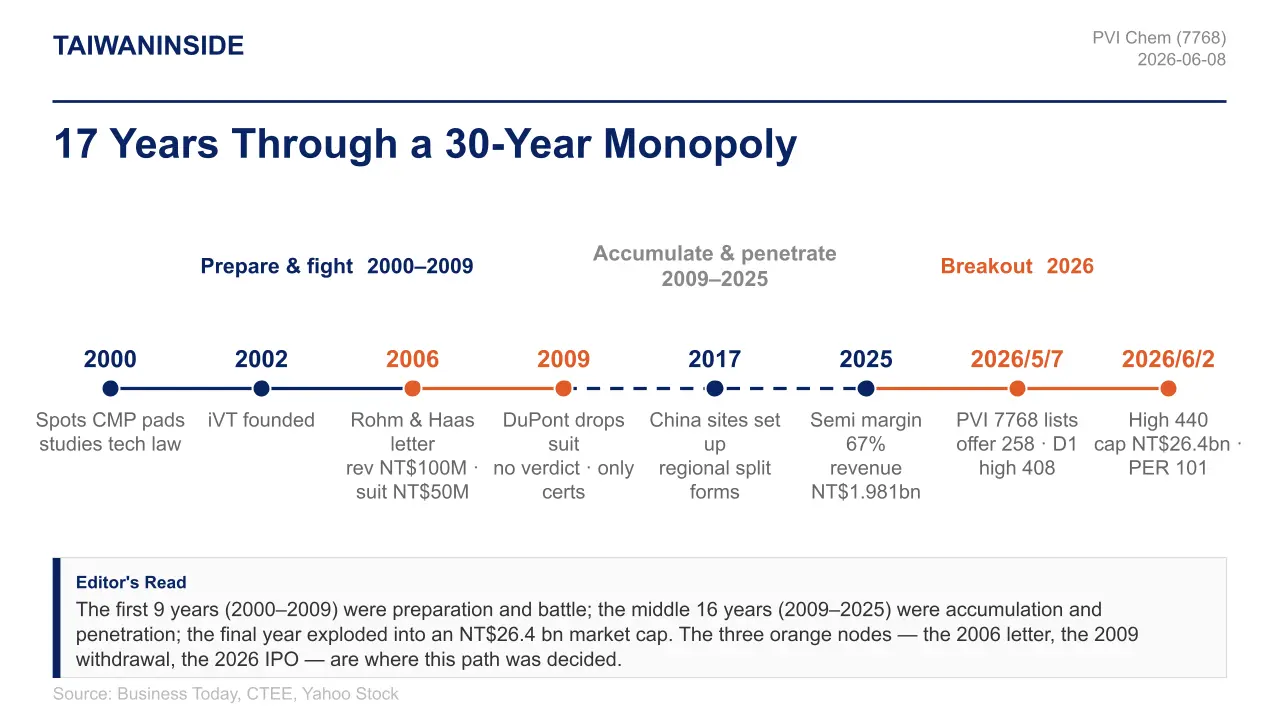

From a Single Lawyer’s Letter to a NT$26.4 Billion Market Cap: The Story Behind PVI’s 67% Gross Margin

A Taiwanese polyurethane (PU) chemicals maker with barely NT$100 million in annual revenue spent NT$50 million fighting a four-year lawsuit. Sixteen years later, it went public at NT$258 a share, surging as much as 58% intraday to NT$408 on its debut and touching NT$440 within a month. The market cap: NT$26.4 billion (≈US$820 million).

In 2006, a lawyer’s letter from Rohm and Haas Electronic Materials—later folded into global chemicals giant DuPont—arrived at the offices of IV Technologies (iVT), alleging patent infringement.

At the time, this subsidiary of Praise Victor Industrial (PVI; TWSE: 7768)—dedicated to producing the CMP polishing pads used in semiconductor manufacturing—had been formally in operation for just two years, with annual revenue of a little over NT$100 million. DuPont, by contrast, had held a 30-year monopoly over the field.

No one expected this small Taiwanese maker, rooted in PU chemistry, to survive even its first year in court.

Why CMP Is So Hard to Break Into: A 30-Year Monopoly in the Polishing-Pad Market

CMP—chemical mechanical planarization—is the most critical “planarization” step in wafer manufacturing.

Think of a chip as a high-rise: before each new floor goes up, the floor beneath must be perfectly level, or the whole structure tilts further with every story. CMP is that leveling step. It relies on two consumables working together: the CMP pad, like sandpaper, provides physical friction; the slurry, like a chemical solvent, drives the reaction. Together they polish the wafer to near-atomic flatness.

Every cycle requires CMP, and a single wafer goes through 20 to 50 CMP steps before it leaves the fab. The number is so high because advanced nodes—with their increasingly complex 3D transistor structures and stacks of more than ten metal interconnect layers—demand extremely precise, layer-by-layer planarization to protect yield. As nodes advance to 7nm, 3nm, and 2nm, the bar for “flat” keeps rising, down to the nanometer. At that scale, the smallest unevenness throws off alignment when the upper layers are stacked, scrapping the entire wafer.

That pushes the technical barrier for pads and slurries ever higher, and the more specialized a company’s products, the more valuable it becomes. Valuates Reports puts the global CMP pad market at US$1.058 billion in 2024, up from US$940 million the year before, and projects US$1.704 billion by 2031—a 7.1% compound annual growth rate.

For the past 30 years, this market has been an oligopoly held by a handful of giants.

DuPont of the United States, Fujibo of Japan, and Cabot of the United States (whose CMP business was folded into Entegris in 2021) carved up most of the global market between them. DuPont still leads the overall market; Fujibo commands a dominant share in soft pads.

Before the 2000s, no Taiwanese company had entered TSMC’s polishing-pad supply chain—until one Taiwanese firm, originally a PU chemicals maker, decided to try.

PVI’s founder, Chu Ming-kuei, was no insider to the tech industry.

In 2000, the first time he saw a semiconductor polishing pad, his first thought was: “Isn’t this just PU? This should be something we can make.” To check, he sought out a TSMC engineer, who told him only: “It can be done—but the big players have it locked up. People have been stuck on it for years, and no one has managed.”

Chu decided to take the gamble. Six years later, as he had anticipated, the lawyer’s letter from Rohm and Haas (later DuPont) arrived—a hurdle he had foreseen and spent years preparing for.

What happened over the next four years rewrote the supply-chain structure for polymer pad materials in Taiwan’s semiconductor industry. PVI’s semiconductor business today carries a gross margin as high as 67%, with customers on both sides of the Taiwan Strait; on May 7 this year it listed at NT$258 and surged as much as 58% intraday to NT$408 on its first day. All of it traces back to that one lawyer’s letter.

A PU Chemicals Maker’s Counterintuitive Move: Law School First, the Factory Later

DuPont, Fujibo, Cabot—the real advantage these three chemical giants held was time.

Getting a polishing pad into a fab is not a one-off sale; it is a long-term, locked-in relationship. Developing a new node—moving from 7nm to 5nm, say—typically takes TSMC two to three years. Throughout that window, the pad supplier moves in lockstep with the fab—tuning formulations, running wafer tests, going through qualification—until the new node enters volume production. Qualifying a single new pad for one node can take hundreds of test runs.

The three incumbents were embedded in this “co-development” mechanism for the long haul, leaving smaller players little room to follow.

Over the past 30 years, the majors and their lead suppliers were bound to one another: DuPont, Fujibo, and Cabot advanced alongside TSMC, Intel, and Samsung through 28nm, 16nm, 7nm, and 5nm. Before each new node, the leading pad suppliers had already designed the next-generation pad, filed the patents, and spent years validating it with customers in the lab.

For any fab, swapping out a supplier it had worked in step with for years was a costly choice.

Years of joint development and built-up rapport are not easily replaced by a newcomer. Even bringing in a new source requires at least 6 to 12 months of qualification, and any delay during that window from poor coordination can leave an entire production line unable to run at full capacity.

Capacity is the one resource a fab can least afford to waste; idling a line over a pad-supplier switch carries an astronomical cost at a time when AI chips are in short supply.

So any newcomer trying to break into a high-end process ecosystem like TSMC’s needs more than passing technology and quality. It needs the patience to wait for the next node’s development cycle and to experiment and validate alongside TSMC over those two to three years. This moat of time was one that, for 30 years, no homegrown Taiwanese supplier had ever crossed.

Chu Ming-kuei refused to accept those rules.

In 1984, he founded Jiuchang Chemical, built on PU (polyurethane) chemistry. In 1986, he formally established Praise Victor Industrial—the parent company (7768) that listed this year—whose early products were tennis-racket grips and internal padding, later expanding into PU goods such as sports insoles and skateboard wheels. In 2002, he set up IV Technologies as PVI’s semiconductor subsidiary, focused on CMP pads.

After the 1997 Asian financial crisis, Chu realized that traditional PU chemistry was at the mercy of exchange rates and product life cycles, and that the company had to move toward “a higher-value industry that could be run for the long term.” The direction he settled on was semiconductors. He believed the team’s end-to-end PU capability—the complete process from synthesizing upstream raw materials to finished downstream products—was precisely what giants like DuPont lacked.

Yet to break into TSMC’s supply chain, the first thing he did was not R&D. It was to enroll in law school.

Chu entered the Graduate Institute of Technology Law at National Yang Ming Chiao Tung University (NYCU)—not for the degree, but to “understand what the patent lawyers were saying.” He knew that against an opponent like DuPont, technology could be left to the team, but if the boss himself did not grasp patent risk, the whole company could be sunk at any moment.

So he spent several million NT dollars commissioning an independent body to produce a detailed patent-clearance report, comparing it one by one against DuPont’s thousands of CMP patents. Before the company even had a finished product, he had hired a dedicated in-house legal expert with a semiconductor background: every groove design and every PU formulation had to be checked against DuPont’s patent list before it could advance to the next stage.

In 2002, he formally established IV Technologies. In 2006, the multinational’s lawyer’s letter arrived, just as expected.

On the Eve of the 2009 Verdict: A Four-Year Lawsuit and a Doctoral Thesis

In 2006, Rohm and Haas (later DuPont) formally filed a patent-infringement suit against IV Technologies.

But that year, IV Technologies’ entire annual revenue was only a little over NT$100 million. The lawsuit was expected to cost NT$50 million—NT$12.5 million a year. Chu did not cut R&D spending or pull back from market expansion in response. He chose to do both at once: fighting the patent litigation he had spent years preparing for, while continuing to send samples to customers and develop the high-spec products TSMC could accept.

Having studied patent law for years, he knew what his opponent was waiting for. DuPont did not need to win the case; it only needed to drag it out long enough that every procurement desk at TSMC and UMC saw the words “IV Technologies carries legal risk”—enough to back Chu into a corner.

The knowledge he had built up at the technology-law institute, and the patent database he had compiled over years, now came into play.

They combed through patent records worldwide and finally found, in one country, a doctoral thesis that had published the relevant technology earlier than DuPont’s patent. They brought the former doctoral student and his advisor to Taiwan from abroad, securing documentary proof.

Then, in court, they did two things: on one hand, proving that IV Technologies’ formulation technology differed from DuPont’s and infringed nothing; on the other, presenting evidence that DuPont’s patent was in fact invalid.

At first instance, IV Technologies won on both counts. DuPont decided to appeal.

The case dragged on for four years, closely watched across Taiwan’s semiconductor industry.

Over those four years, IV Technologies did not retreat and DuPont did not give up; each side’s legal team amassed thousands of documents. If Chu lost, IV Technologies would be kicked out of the semiconductor supply chain for good. If he won, it would be the first non-US, non-Japanese maker in 30 years to dare to challenge DuPont in this product category—and survive.

Premium Members Only

This is a premium article. Please join our membership to read the full content.

Become a member to unlock all in-depth reports and exclusive analysis.

Already a member? Login Now

Related Articles

Backed and Led by Stan Shih: A Capacitor-less DRAM Startup Takes On the Big Three's Thirty-Year Order

No Accident: How Taiwan’s Small Equipment Makers Secured a Critical Role in TSMC’s AI Packaging Process While Global Giants Stayed Away

The Wealth of a Tech Island: Decoding Taiwan's "Thousand-Dollar" Stock Surge and One Veteran Investor's $300M Masterclass