From Broadcom to MediaTek: The Design Hub for Custom AI Chips (ASICs) Is Quietly Shifting Out of the US

On June 3, Broadcom posted record AI revenue—yet its stock fell hard the same day. A slice of the custom-ASIC business at Broadcom's largest customer, Google, is being taken by a rival from Taiwan: MediaTek. Broadcom's challenge is also the new landscape now facing the entire IC-design industry under the intense competition of AI.

Broadcom's Earnings: Google's Orders Get Split Up

In early June, global equities sold off and the Philadelphia Semiconductor Index (SOX) corrected sharply. Two triggers set off the slide. The first was Broadcom's second-quarter earnings, released on June 3.

It was one of Broadcom's strongest quarters in years: revenue of US$22.2 billion, up 48% year over year, with AI-related revenue of US$10.8 billion, up 143%—a record high.

But alongside the record numbers, Broadcom also faces stiff competitive pressure: its major customer Google has split its orders among multiple suppliers, and one important rival is Taiwan's leading IC-design house, MediaTek.

The second trigger was a SemiAnalysis forecast that Nvidia would cut memory content in its next-generation servers. The call briefly hammered memory stocks, but the "memory cut" reading was a market overreaction and a misinterpretation—Nvidia trimmed the per-rack configuration in order to spread the same memory across more racks, so total usage did not fall. Attention then shifted to how the ASIC and IC-design-service market would rise, fall, and reshape itself.

Broadcom, a Decade-Long Champion with Six Core Customers

An ASIC is a chip purpose-built for a single task: in that task it clearly outperforms a general-purpose GPU, but it cannot handle work outside its purpose.

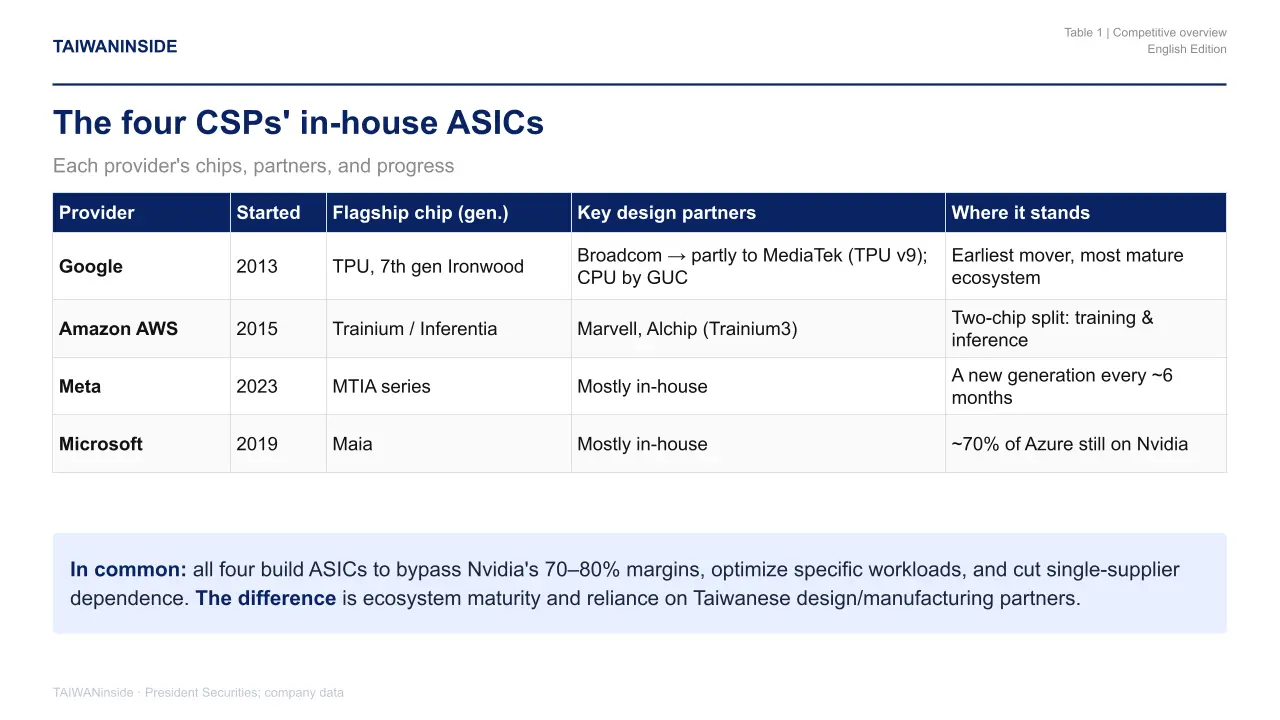

To review the ASIC industry, a good starting point is the investment pace of the four major CSPs (cloud-service providers)—Google, Amazon, Meta, and Microsoft—and how it has reshaped the market.

The four CSPs are building ASICs for roughly three reasons. First, cost control: in-house chips bypass Nvidia's 70–80% gross margins. Second, performance optimization: an ASIC is markedly more efficient than a general-purpose GPU on a specific workload. Third, supply-chain autonomy: the 2023–2024 GPU shortage taught these giants the risk of depending on a single supplier.

Broadcom has long been the king of ASICs. Beyond a decade of cooperation with Google, it holds six core custom-chip customers, including Anthropic, Google, Meta, and OpenAI.

Once a customer hands its chip design to Broadcom, everything from architecture and verification to back-end packaging is locked together; switching suppliers means redesigning the whole chip. In a segment long dominated by the US, an Asian company breaking into Google's core orders is a rare event of the past few years.

MediaTek Breaks into Google's TPU via SerDes

Google's TPU partners were once led by Broadcom; today, part of that business has shifted to MediaTek, while Google's CPU partner is Global Unichip (GUC). MediaTek and GUC won their openings not only because of strong design-and-manufacturing capability, but also because they set gross margins lower than Broadcom's, work flexibly with customers, and maintain close ties with foundry TSMC—all decisive reasons for landing the orders.

One concrete example is Google's next-generation TPU v9: reports say MediaTek won the order on the strength of its 448G high-speed-transfer (SerDes) technology, targeting a 10–15% share. It is the first time in a decade that an Asian rival has broken into Broadcom's most core customer.

Is Broadcom really unable to hold the line—or is this just a momentary slip? That depends on exactly how much of the Google business has shifted, and how fast.

Google TPU: Broadcom's Share Falls from 95% to 65%

First is Google—the earliest mover and today's frontrunner. Google's TPU program began in 2013 and has reached its seventh generation; the eighth is slated for the third quarter of this year.

Google built the TPU after realizing that running a neural network on every search query would demand an enormous number of chips, pushing it toward purpose-built matrix-multiplication silicon. The TPU was initially for internal use only, powering services such as voice search, image recognition, and real-time translation.

On the technical side, Google's seventh-generation Ironwood packs 192GB of HBM3E memory per chip with bandwidth up to 7.37 TB/s, and Anthropic has committed to taking up to one million units. The TPU ecosystem is also replicating Nvidia's CUDA lock-in: code optimized for the TPU on JAX or TensorFlow is very costly to migrate elsewhere, and every new deployment makes the TPU harder to replace.

The shift in TPU manufacturing orders has been gradual. Foreign brokerages estimate Broadcom's share of Google's TPU at about 95% in 2026, falling to about 80% in 2027 and about 65% in 2028. MediaTek is steadily absorbing the difference, and MediaTek's own earnings calls show Broadcom's grip loosening: on its Q1 2026 call it doubled its full-year AI-ASIC revenue target to US$2 billion and confirmed the Google TPU program was on track.

Looking across the field, each company has taken a different path with different strengths and different partners—and over time, the work has gradually moved from US firms to Taiwanese ones.

Not just Google. Amazon, Tesla, and even Musk's space program have, over the past few years, handed chip design to Taiwan's MediaTek, GUC, and Alchip. But the Taiwanese firms taking these orders run gross margins far below those of Broadcom, which holds the key IP. Is this a genuine shift in the global AI-hardware map—or is Taiwan, once again, simply grabbing the low-margin layer as production needs rise and products multiply?

Amazon AWS: a US$364 Billion AI Order Backlog

Premium Members Only

This is a premium article. Please join our membership to read the full content.

Become a member to unlock all in-depth reports and exclusive analysis.

Already a member? Login Now

Related Articles

Samsung stopped the bleeding with sky-high bonuses; TSMC has no union, yet no one cries foul. What makes the two systems so different?

Cutting Procurement Costs by Twenty Percent, Turning Every Life into Data: Four Key Lessons Ukraine’s Defense Reform Holds for Taiwan

Intel's Pool Is Still Cold — and Musk's May Be Even Colder. C.C. Wei Says Samsung Is "Dreaming." So How Would Morris Chang Have Judged TSMC's Rivals?